|

|

|

|

|

|

|

|

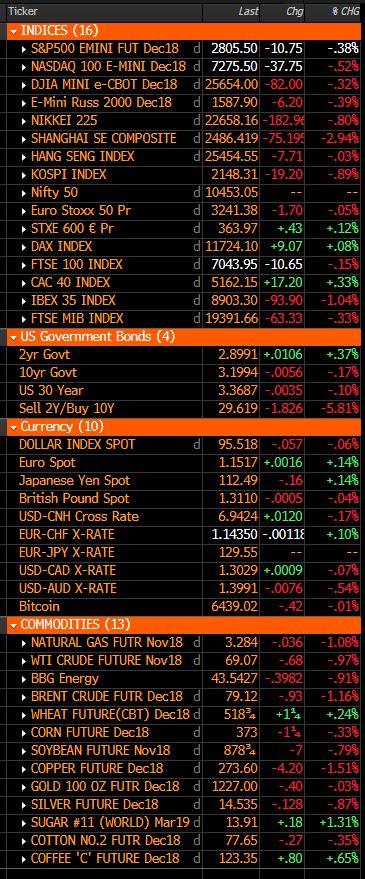

- China the big negative outlier -3%; otherwise Japan -.8%, Europe flat and S&P futures -10 and in the middle of a 15 point range. However, US still up sharply for the week thanks to big Tuesday rally. Treasuries weaker across the curve. Dollar weaker vs both euro and yen. Gold flat. WTI crude down 1%, extending this week’s

pullback.

- China selloff seems focused on concerns about forced liquidation in shares pledged as collateral for loans. Bloomberg saying margin calls accounted for much of the selling ($600B/11% of the market cap is pledged as collateral). Yuan weakness another headwind. As expected, Treasury did not label China a currency manipulator, but some thoughts that gives Beijing room for more depreciation. Structural deleveraging push has been big headwind on growth momentum, while trade tensions with US lasting longer than expected.

- Not a lot going on elsewhere. Hawkish takeaways from FOMC minutes continue to reverberate, though likelihood of it taking the funds rate above neutral has been widely discussed before. Trump talked about spending cuts on Wednesday. Ross expressed frustration with lack of progress on US-EU trade talks. Like Kudlow, downplayed prospects for anything out of possible Trump-Xi talks next month. McConnell called for progress on trade talks.

- Italian budget saga remains on the radar, though few fresh developments today as PM Conte said he expects criticism from the EU over budget but will explain the details. Der Speigel on Wednesday reported EU Commissioner Oettinger said it’s very likely Rome’s budget plans will be rejected.

- The FT cited UK PM May, who confirmed overnight reports that UK is considering extending Brexit transition period. Initial reports said implementation period could be extended until end of 2021, but May insisted it is likely to be for several months and her intention is for a new UK-EU relationship to take effect at the end of 2020.

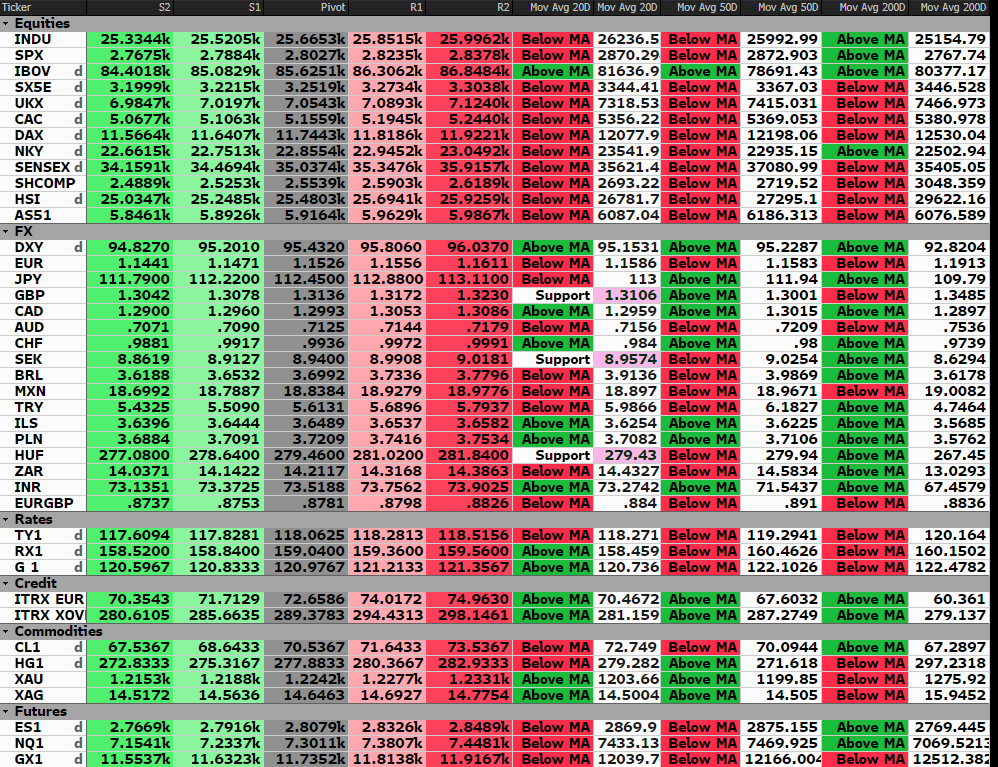

- Higher US rates again getting attention; the US 10 Yr yield is +5 bps in 2 days (3.21%) and within 4 bps of new seven year highs.

- Post Fed minutes, Fed Funds futures still showing a 78% chance of another hike by December (that percentage has remained unchanged despite the recent equity weakness).

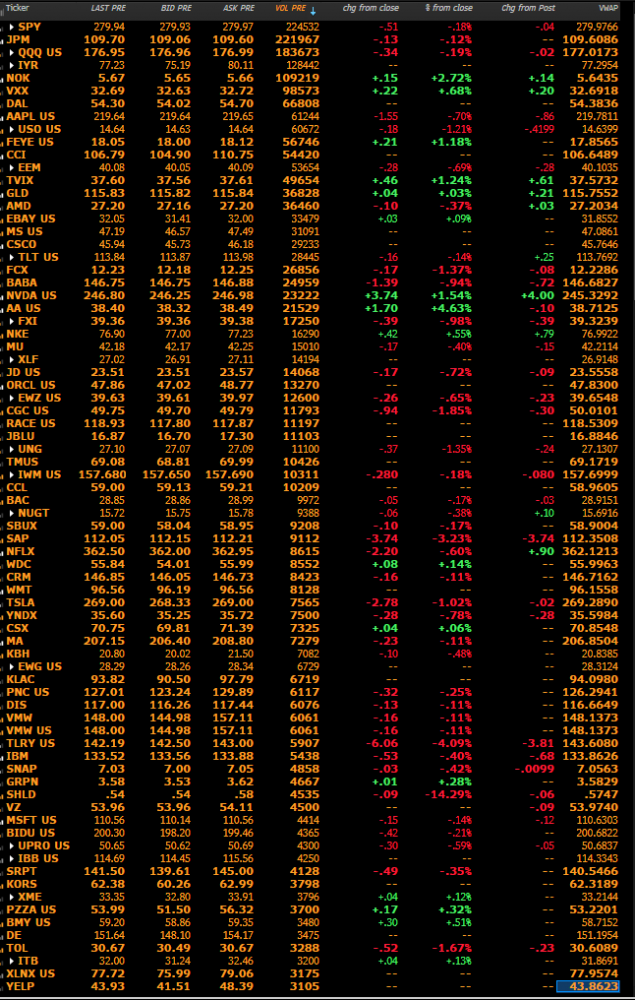

- An Q3 earnings read; 67 S&P names have reported so far with 64% (well below Q2) beating Revenue estimates and 86% better

on the EPS line.

- Earnings activity continues to pick up. Growth and beat rates look good, but bar has been higher. TXT missed on softer industrial segment. URI beat, but pricing missed and guidance raise disappointed. AA beat on EBITDA and announced $200M buyback. SEE negatively preannounced and guided 2018 below. STZ CEO stepping down.

- Main focus today will be on the EU Leader’s Summit (10/18-19), Fed speakers (Bullard, Quarles), and earnings (ADS, BBT, BK, DHR, DOV, GPC, KEY, LNN, NUE, PM, PPG, SNA, SON, TRV, TSMC, TXT,

WBC, and WBS before the open and ASB, AXP, BXS, CE, CP, EBAY, ETFC, ISRG, PBCT, PYPL, LLNW, OZK, and WERN).

|

|

|

|

|

|

|

US Economic Reports For The Rest Of The Week

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Any comments, suggestions, or questions - please email info@hedgefundtelemetry.com

Occasionally, an earnings report date could change, or could be incorrect. We rely on various sources including Street Account,

Factset, and Bloomberg to compile this report.

|

|

|

|

|

Know which button to push next

in the market.

|

|

|

|

|

|

Unsubscribe me from Hedge Fund Telemetry

CONFIDENTIALITY NOTE and DISCLAIMER: This message is for the named person's use only. It may contain confidential, proprietary or legally privileged material. No confidentiality or privilege is waived by any accidental or unintentional transmission. If you receive this message in error, please immediately delete it and all copies of it from your system, destroy any hard copies and notify the sender. You must not, directly or indirectly, use, disclose, distribute, print or copy any part of this message if you are not the intended recipient. Hedge Fund Telemetry LLC. cannot guarantee the

confidentiality of the material transmitted; therefore, information of a sensitive or confidential nature should not be transmitted. There is risk in trading markets. Hedge Fund Telemetry reports are based on information gathered from various sources and believed to be reliable, but are not guaranteed as to accuracy and completeness. The information is subject to change without notice and Hedge Fund Telemetry LLC has no obligation to provide any updates or changes. Hedge Fund Telemetry LLC is providing this data for informational and educational purposes and does not believe that it is sufficient to base an investment decision on. This information should not be regarded as a solicitation or recommendation of any particular security or to engage in any trading strategy. One should always check with your licensed financial advisor to determine suitability of any investments.

|

|

|

|

|

|

|